How much of a difference does fintech API make? Take a trip back a few decades, banking was a wholly different field. Banking was straightforward yet restrictive, centered around in-person branch visits for financial tasks. Cross-collaboration between financial, and especially non-financial, institutions was rare, offering customers a limited range of services.

Fintech APIs have transformed the scene entirely, connecting disparate entities, allowing varied software systems to interact seamlessly, introducing a new level of convenience, and expanding what's possible in finance. When you access an app to check your finances from multiple bank accounts, APIs seamlessly pull and consolidate all financial data for you. Or when it's time to make quick and secure online payments, API open banking applications allow you to do it directly. So, now, when you easily transfer funds through your favorite budgeting app, or when a business instantaneously processes payments via an online platform – remember, it's the power of fintech APIs that makes these experiences possible.

They've become the backbone of innovation with 65% of traditional financial institutions having entered at least one fintech partnership. Many of these collaborations were heavily reliant on the use of banking APIs to facilitate their offerings.

Fintech APIs serve a multitude of purposes:

- Easy and quick peer-to-peer money transfers.

- Instantaneous business payment processing.

- Swift access to credit scores and account verification.

- Advanced insights for personalized insurance underwriting through IoT data.

- Access to financial histories and real-time market data, aiding strategic decision-making.

In this blog post, we will take you through the all use cases, payoffs, and challenges of fintech API integration, and successful examples of those that are driving this innovation, shedding light on APIs' crucial role in redefining modern finance.

What is fintech API and why it's important?

Fintech open banking APIs, or application programming interfaces, are virtual bridges that allow distinct financial software systems to interact and share data securely across the internet. They work by enabling an authorized application to send a request to a bank's system. The bank's API confirms the legitimacy of the request and then facilitates the exchange of data.

In simple words, APIs make data communication between different applications and software systems possible, easy, and efficient. They work as a gateway that receives requests, processes them, and delivers the necessary information to the recipient. APIs are valuable for the FinTech industry, providing access to vast financial data and services.

APIs go hand in hand with the concept of open banking, the practice of sharing data across various financial institutions. Traditional systems often struggle with fragmented data, limited information access, and manual procedures. However, APIs effectively address these issues. APIs are the technological foundation that makes open banking possible and helps banks in several ways:

- Financial institutions can collaborate with third-party developers to create tailored financial services, products, and applications that cater to specific consumer needs and preferences.

- They provide a seamless banking experience, meeting modern consumers' demand for quick, digital financial services.

- By enabling rapid credit assessments and verifications, banks can expedite their processes and improve customer experiences.

- Access to more comprehensive customer data allows banks to create personalized products and efficient risk management strategies.

- Real-time financial insights empower banks to adapt quickly to the market, leading to better investment decisions and financial strategies.

Collaboration with third-party developers through APIs champions innovations like payment processing solutions from Stripe or PayPal, enhance secure and seamless transactions without the need for websites or apps to directly manage banking details. This integration extends to non-financial platforms, where financial services become part of the everyday user experience. Notable examples include:

- E-commerce platforms that implement built-in payment solutions for seamless checkout experiences.

- Ride-hailing apps that provide in-app financial management tools, allow users to monitor their ride expenses.

- Social media sites that have added payment services enable direct money transfers and purchases within the platform.

- Food delivery apps, many of such now include built-in wallets, provide the flexibility to order food and keep track of expenses within the same platform.

- Healthcare payment systems that can process payments for services or integrate health savings account management through APIs.

- Insurance claim processing – some apps are leveraging APIs to facilitate the filing and processing of insurance claims directly through mobile or web applications.

The examples of open banking influencing various sectors are numerous and ever-growing, and so are its accolades. From a personal finance dashboard navigation to streamlined loan applications and innovative payment solutions, open banking is transforming the financial landscape. These indicators underscore the expanding influence of open banking and the critical role of APIs.

How fintech APIs work

Fintech APIs serve as communicators between different software systems. When using a financial app, it leverages APIs to access your data from connected banks or financial services. The process is secure; APIs function like encrypted digital messengers, carrying requests back and forth using complex 'keys' or codes that allow only authorized exchanges.

The process is as follows:

- Request Initiation: A user initiates a process, such as checking their balance through a financial app.

- API Call: The app sends an API call, which is a request for data or an action, to the user's bank.

- Verification: The bank's API verifies the request using secure authentication protocols.

- Data Retrieval: Once verified, the bank’s API retrieves the requested information.

- Response: The API sends the information back to the requesting financial app.

- Display: The app receives the data and displays the updated balance to the user.

3 types of fintech APIs

There are three primary types of APIs – case, each offering a different level of accessibility and data-sharing capabilities tailored to specific use cases:

- Private APIs are designed for internal use within an organization. They enable different departments or teams to share data and interact with internal software applications efficiently. Private APIs not only improve collaboration but also ensure data security as they are inaccessible to external entities.

- Partner APIs are shared with specific external partners or VIP customers. These APIs create a controlled gateway for partners to interact with the organization’s data or services, providing a balanced mix of accessibility and security. Headless API systems are usually the best solutions for interacting with external parties as it provides backend functionality while working with different designated interfaces. Partner APIs are often used in business partnerships or collaborations where data exchange is crucial.

- Public APIs, also known as open APIs, are made available to the public, allowing any third-party developers to use and build upon the organization's data or services. Public APIs can foster innovation, increase brand visibility, and attract broader developer engagement.

Use cases of fintech APIs

Finastra reveals that 70% of banks are leveraging open banking APIs to widen their customer base. Startups like Mint utilize these APIs to give users a unified view of their finances and tailored money management advice. Similarly, Stripe and Square have harnessed these tools to streamline e-commerce and payment processing, proving invaluable for both SMEs and large enterprises.

Fintech APIs offer a range of applications that touch nearly every aspect of personal and business finance.

Embedded payments

Embedded payments utilize API technology to knit payment functionalities directly within apps or software, eliminating the need to navigate to external payment processors. This embeds the transaction process within the user’s journey on a particular platform, allowing for a more streamlined and cohesive experience. By integrating APIs from payment service providers, businesses can securely handle transactions, authenticate users, and manage funds without the friction of traditional payment methods. In technical terms, the API works by facilitating real-time data exchanges and ensuring secure payment tokenization, thereby maintaining a high level of security while providing the convenience of in-app or in-platform purchases.

Example: A retail app uses a payment API (e.g., Stripe) to process customer purchases directly within the app, offering a smooth checkout experience without redirecting users to external payment gateways.

Banking as a service (BaaS)

These APIs allow non-bank businesses to add banking features to their offerings, transforming the way customers interact with financial services. From opening bank accounts to providing debit cards and loan services, BaaS expands financial services accessibility to a broader audience.

Example: A personal finance app (e.g., using Plaid) allows users to connect their bank accounts, enabling features like balance checks and fund transfers directly within the app, without logging into separate banking portals.

Personal finance management (PFM)

Budgeting apps, investment tools, and even robo-advisors rely on APIs to securely access and analyze your financial data. This integration allows PFM tools to aggregate and analyze your financial information in real-time, providing you with a comprehensive view of your financial health. By leveraging APIs, PFM platforms can offer personalized financial advice, budgeting help, and spending insights, all tailored to your specific financial situation.

Example: Budgeting apps (e.g., Mint) aggregate financial data from various bank accounts and credit cards, categorizing expenditures to provide users with insights into their spending habits and suggesting ways to save money.

Lending and credit

APIs fuel digital lending and credit services by connecting lenders to borrower's financial data. They provide real-time access to crucial data like employment history, income, credit scores, and more. This helps lenders quickly assess a borrower's creditworthiness and make informed lending decisions. Additionally, APIs streamline processes such as loan application, disbursement, repayment, and tracking, creating seamless digital experiences. It’s safe to say that APIs have transformed lending and credit from a slow, paperwork-heavy process into an efficient, user-friendly digital service.

Example: An online lending platform uses credit scoring APIs (e.g., Experian) to assess loan applications automatically by retrieving and analyzing applicants' credit histories, dramatically reducing the decision-making time.

Crowdfunding

APIs in crowdfunding make it super easy for platforms to connect with payment systems, social networks, and other services. They help users create campaigns, share with friends, and handle payments all in one place. So, if you've got a cool idea or a cause you care about, APIs help you raise the funds you need quickly, securely, and conveniently.

Example: Launching a crowdfunding campaign for an eco-friendly water bottle, can APIs help you share it on social media and securely collect funds through services like PayPal or Stripe – all in a few clicks.

Investment and wealth management

Investment APIs democratize access to financial markets, enabling users to buy, sell, and manage stocks, bonds, and other securities. Robo-advisors use these APIs to create personalized investment strategies, making wealth management services accessible to all investor levels.

Example: Robo-advisors (e.g., Betterment) use investment APIs to access market data and execute trades, offering personalized portfolio management based on the user's risk profile and financial goals.

Insurance tech (InsurTech)

Fintech APIs in the insurance sector streamline the process of buying insurance, claiming processes, and managing policies. They enable customized insurance packages based on user data and automated claims processing enhances operational efficiency and customer satisfaction.

Example: Digital insurance platforms integrate with APIs (e.g., Lemonade) to automate the quoting process, using personal data to tailor insurance packages and process claims faster through data analysis and automation.

Cross-border transactions

With the help of APIs, financial institutions can offer more efficient and less costly cross-border payment services. This includes real-time currency conversion rates, reducing the complexity and costs associated with international transactions.

Example: Payment services (e.g., Wise) use currency exchange APIs to offer customers real-time exchange rates and low-fee international money transfers by matching transactions in different currencies within the same geography.

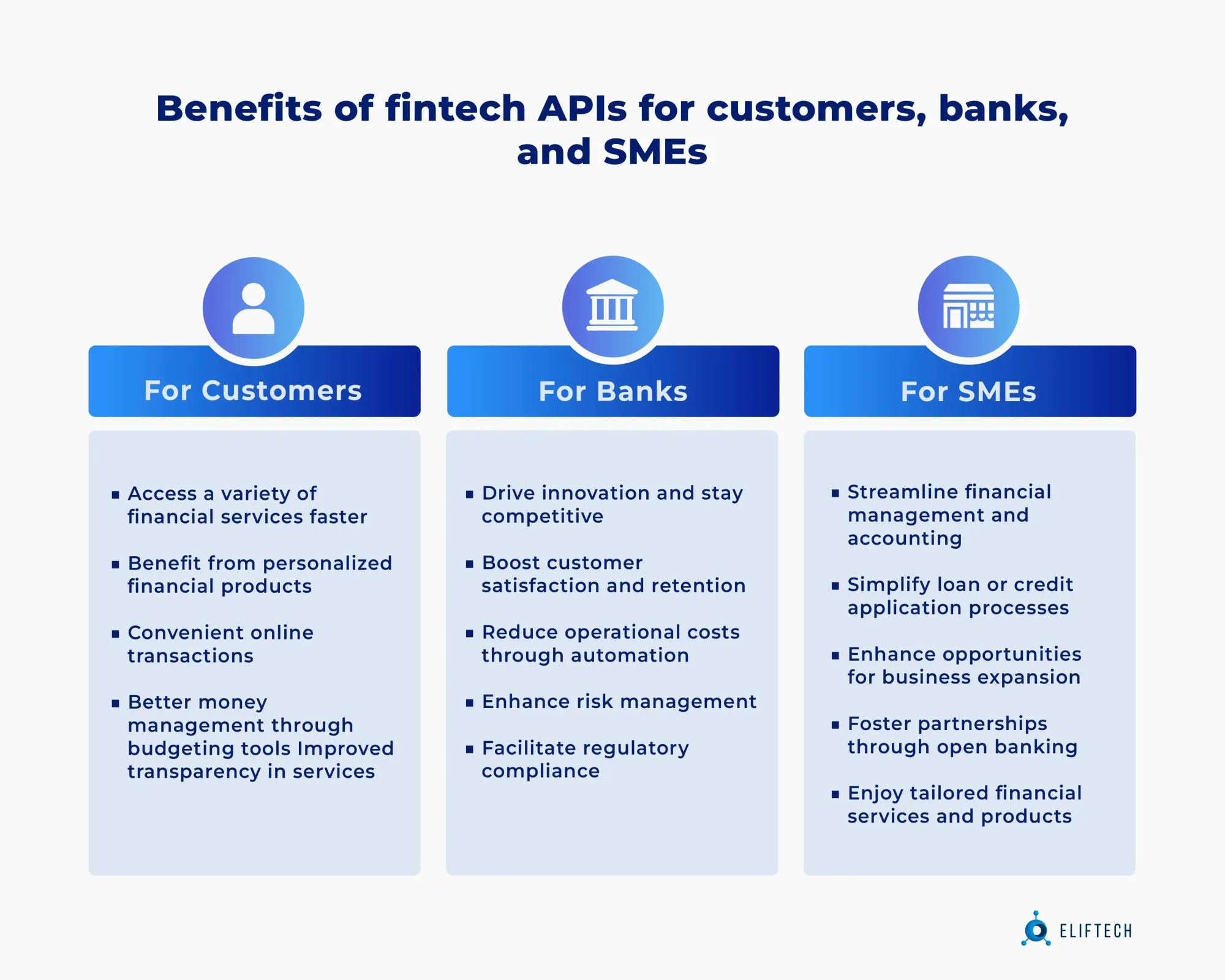

Benefits of fintech APIs

By 2025, the banking sector anticipates a tripling in API usage, signaling a technological tide that's transforming the industry. Developers also provide insight, with 56% asserting that APIs elevate their products' capabilities. They also mark:

- Accelerated innovation (52%)

- System integration (40%)

- Tangible business value (36%),

- Them acting as standalone products (22%).

Yet, we're just scratching the surface. APIs in fintech apps go further.

Improved user experience

APIs in fintech connect different services, sync data in real time, and keep everything running smoothly. This means users can swipe, tap, and check on their finances without hitting snags or seeing outdated info. It's like having a financial assistant in your pocket – your apps just 'get' you and your needs, thanks to APIs smoothly exchanging data under the hood. Quick, secure, and tailored to you – that's the user experience APIs are delivering in today's fintech apps.

Secure data exchange

APIs act as encrypted messengers, ensuring that every piece of information shared between apps and services is locked tight in a virtual vault – only accessible to those with the right key (that's you and the intended service). This setup keeps prying eyes out and safeguards your financial details, whether you're checking your bank balance, making a payment, or investing. APIs are the silent guardians in the digital finance world, making sure your data moves safely across the internet’s vast expanse.

Lower development costs and rapid development of new features

By offering ready-made blocks of code that easily integrate with existing systems, APIs eliminate the need for developers to reinvent the wheel every time they want to add a new feature or service. With the integration of AI in fintech and API tools, institutions and businesses can focus on streamlining complex processes. This means less time (and money) spent on development and testing, as the heavy lifting has already been done. For fintech startups and established companies alike, this can lead to significant savings, enabling them to allocate resources more effectively elsewhere.

Compliance with regulatory requirements

APIs come designed to align with the latest regulations – think GDPR, PSD2, or KYC practices. So when a fintech app plugs into one of these APIs, it's plugging into a system that's already set to play by the rules. This saves time and resources that would otherwise go into tracking changes in law and adjusting the code accordingly. Plus, as regulations evolve, API providers update their offerings, making it easier for fintech services to adapt and remain on the right side of the law with minimal fuss.

5 challenges of fintech API integration

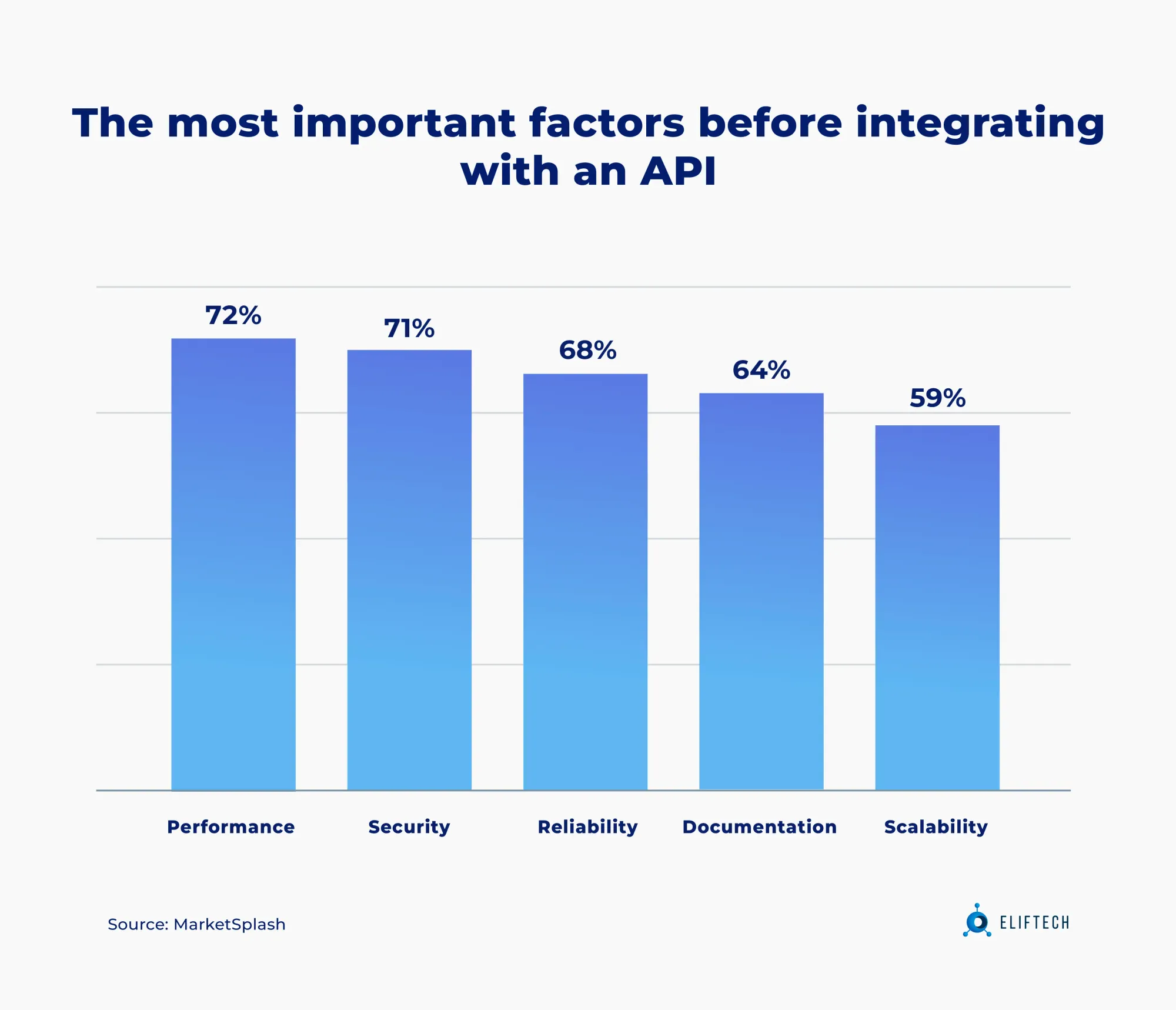

When integrating with an API, prioritize these key factors: performance (72%), security (71%), reliability (68%), documentation (64%), and scalability (59%).

1. Security

Security sits at the forefront of fintech concerns, especially considering that APIs grant access to vast pools of sensitive financial information. According to industry insights, 48% of FinTech companies list API security as their principal concern. Reflecting the apprehension around API vulnerabilities, more than 50% of firms have delayed the launch of new APIs due to security issues. Surprisingly, over 80% of respondents lack confidence in their existing tools to thwart API attacks. The path to securing these digital gateways involves implementing robust encryption protocols, conducting periodic security audits, and maintaining vigilance through continuous monitoring to identify and mitigate potential threats effectively.

2. Compliance

Aligning with financial regulations and data protection laws is another steep hill to climb. The fintech sector is heavily regulated, with legislations like GDPR in Europe and CCPA in California setting stringent guidelines for handling personal and financial data. Businesses must ensure that their API integrations comply with these ever-changing regulations to avoid substantial fines and reputational damage. The complexity of compliance is heightened by the global nature of fintech services, where APIs must meet the legal requirements of multiple jurisdictions.

3. Technical complexity

One of the most significant challenges in integrating fintech API arises from the technical complexity involved in aligning disparate systems into a cohesive, functional, and scalable whole. This challenge can be mainly attributed to three key factors:

- Interoperability and standardization: With hundreds of fintech APIs available, a lack of standardization can pose integration challenges. The diversity in code languages, data formats, and protocols can complicate the process of integrating multiple APIs into one platform. For instance, an API written in JavaScript might not easily interact with a system coded in Python. Similarly, APIs designed for RESTful communication might not be compatible with a SOAP-based system.

- Scalability: Scalability relates to an API's ability to maintain performance and availability levels as demand increases. Given the dynamic nature of the fintech sector, businesses must ensure their API-based services can handle peak demand periods without compromising user experience.

- Documentation & support: Adequate documentation and reliable support from the API provider significantly impact the ease of integration. For example, poorly written, incomplete, or outdated API documentation can confuse and slow down developers, resulting in delays and mistakes in API integration. APIs with complex integration requirements need straightforward, accessible, and extensive documentation to aid developers in the process. Additionally, timely technical support is crucial for troubleshooting and resolving integration issues to minimize disruption.

Legacy system integration

Many financial institutions operate on legacy systems that are not inherently designed for modern API integration. The challenge here involves creating interfaces or middleware that allow these older systems to communicate effectively with new API-driven technologies without compromising security or efficiency.

Expertise in API design and development

2023 State of the API Report by Postman

API integration is not just about connecting two systems; it requires a deep understanding of both the technical and business aspects to design seamless, efficient, and secure integrations. The scarcity of skilled API designers and developers who can navigate these complexities can lead to suboptimal API designs that fail to meet the intended objectives or compromise on performance, security, and scalability.

How fintech API connects the fintech ecosystem

APIs are changing the game in fintech, making it easier for both new and established players to add cool features to their offerings without having to build these systems from the ground up.

For financial institutions, APIs are a big win – they speed up innovation, cut costs, and make customers happier with better, more personalized services. They turn data into valuable insights, helping companies make smart moves. Plus, dealing with complex financial rules gets simpler, and spotting fraud becomes quicker, keeping everyone's money safer.

Through APIs, fintech firms can integrate functionalities like payment processing, fraud detection, and real-time analytics into their offerings.

In the analysis of the top 10 open banking platform providers in fintech 2023 by Fintech Magazine, we can see firsthand how these companies reinforced their offering with APIs:

- Plaid: Can integrate over 12,000 financial institutions, enabling 8,000+ fintech services.

- Stripe: Powers global payment for various platforms like Salesforce and Shopify.

- Token: Achieved 80% bank connectivity in 16 European markets promoting instant, affordable payments.

- TrueLayer: Europe's leading open banking payments network, enabling swift transactions for partners like Freetrade and Coinbase.

- Salt Edge: Facilitates smarter digital services like SME lending and digital accounting.

- Bud Financial: Processes 300 million transactions a month aiding financial decision-making.

- DirectID: Aids in smarter credit and risk decisions by providing financial insight to lenders.

- Yodlee: Utilized by 1,500+ financial institutions and fintech companies, serving 30 million customers.

- Finflux: Built a US$9bn loan portfolio, serving over 20 million borrowers in 15+ countries.

- Tink: Managed a billion API calls a month and powered over 300 banks and fintechs with around 6,000 integrations.

Traditional banks ventured into the API and have found a path to stay relevant and competitive amid the digital disruption. Traditional banks and fintech startups are crafting a surprisingly symbiotic relationship.

- J.P. Morgan Chase partnered with the fintech company OnDeck to use its platform for underwriting loans for small businesses. This partnership allowed J.P. Morgan to expedite loan processing and offer a better digital experience.

- Another example is BNY Mellon which worked with Fintech Sandbox, a nonprofit that provides fintech startups with access to financial data and infrastructure, to create new investment solutions and drive innovation.

- HSBC engaged with Bud Financial to enhance its digital banking services. Bud’s aggregation software and marketplace were integrated into HSBC’s mobile banking app, giving customers a panoramic view of all their finances and allowing HSBC to recommend more personalized financial products.

The myriad of connections between financial services, payments, and eCommerce APIs, illustrate how they have rapidly evolved and expanded. The diversity and number of these APIs underscore the endless possibilities for connecting various segments of the fintech ecosystem, including insurance, accounting, and marketplaces, showcasing a vibrant and interconnected digital financial infrastructure that's set to propel the industry's future.

How to successfully integrate fintech API

Institutions looking to harness the power of fintech API often confront a host of challenges we discussed earlier, from the lack of API design skills to integrating these digital tools into clunky legacy systems. Furthermore, sometimes the necessity of modernizing these legacy systems is a pivotal step toward smoother API integration, requiring the other set of skills from API developers.

Solution? Tech partners can offer expert guidance and practical solutions for overcoming these challenges.

- Offering custom API development, tailored to the specific needs of the institution.

- Developing a comprehensive approach to managing the full API lifecycle, ensuring security, performance, and scalability.

- Modernizing outdated systems to facilitate easier integration with APIs.

- Implementing robust security measures to protect data and maintain compliance with financial regulations.

- Collaborating with established API providers to leverage their cutting-edge technology and experience.

Leveraging over a decade of expertise in fintech software development services, ElifTech has the right skills to deliver seamless fintech API integration. Our approach not only ensures flawless incorporation of APIs into existing systems but also guarantees strict adherence to regulatory standards.

Through our strategic partnerships with industry leaders Dwolla and Stripe, we're empowered with a robust suite of financial tools. This enables us to embed sophisticated payment processing capabilities seamlessly into the solutions we craft for our clients. For further details or to discuss our offerings, engagement models, and technology stack, feel free to reach out for a detailed consultation.